Bored Apes, Moonbirds to feature on NFT-customized Mastercard debit cards

The customizable card will only support NFT avatars from select blue chip collections, subject to Mastercard’s design standards and an owner verification process.

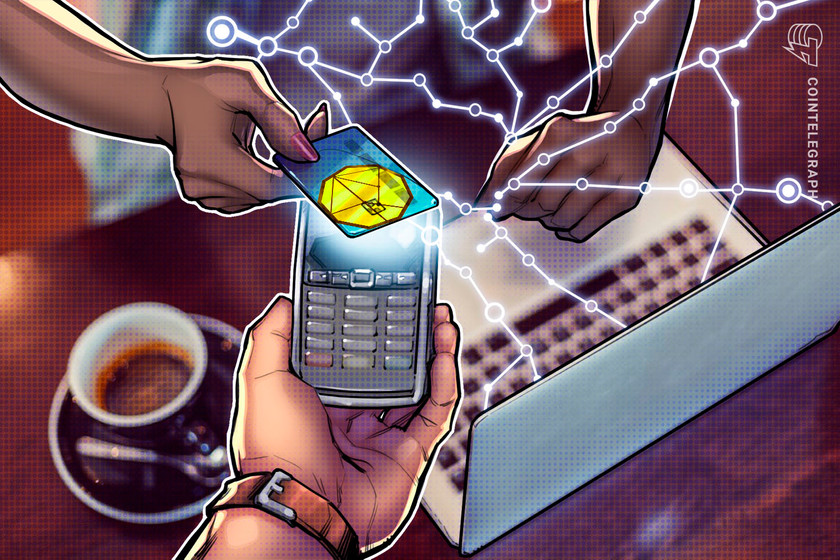

Mastercard has launched customizable nonfungible token (NFT) debit cards, allowing some cardholders who own avatars from select NFT collections to add the artwork onto the payment card.

The debit cards are made available through a Monday partnership with the European cryptocurrency exchange platform hi, allowing its Gold members to personalize their debit cards with an NFT they verifiably own.

Gold membership with the platform is obtained by staking a minimum of 100,000 hi Dollar’s (HI), the platform’s native token, a sum worth around $4,600, according to data from CoinGecko.

NEWS! Today @hi_com_official launches the world’s first debit card featuring NFT Customization, allowing cardholders to personalize the face of their card with an NFT Avatar. Read more here https://t.co/awNVowcsuG pic.twitter.com/A5xFsHlX0w

— Mastercard Europe (@MastercardEU) September 26, 2022

The cards will allow spending in fiat, stablecoins or any cryptocurrency the user holds and is accepted wherever Mastercard is available. Other features such as hotel credits, cash back incentives and rebates on Netflix and Spotify subscriptions are also touted as benefits of certain membership levels.

Mastercard’s crypto and fintech enablement vice president, Christian Rau, said with consumer interest in NFTs and crypto growing the payments provider was “committed to making them an accessible payments choice for the communities who wish to use them.”

A limited range of NFT collections will be supported including CryptoPunk, Moonbirds, goblintown, Bored Ape and Azuki, owners of these NFTs will have to become Gold members with hi and verify their NFT ownership with the platform to receive their custom cards.

Additionally, the cards are available only within 25 European Economic Area (EEA) countries and the United Kingdom.

Related: Innovation will drive NFT adoption despite mainstream presence: NFTGo founder

With the wider downturn in crypto markets over the last few months, most of the “blue chip” NFT collections took a price hit, but data by NFTGo shows the performance of blue-chip NFTs growing steadily since Sept. 12 possibly bringing renewed interest to the largest collections.

Mastercard has helped crypto payments go mainstream with its support for the assets, even allowing Mastercard holders the ability to purchase NFTs through partnering with multiple NFT marketplaces in June.